-

- Downloads

There was a problem fetching the pipeline summary.

Add documentation for basic of PE

parent

eaf8d4d7

No related branches found

No related tags found

Pipeline #

Showing

- docs/basics-of-parameter-estimation.txt 113 additions, 0 deletionsdocs/basics-of-parameter-estimation.txt

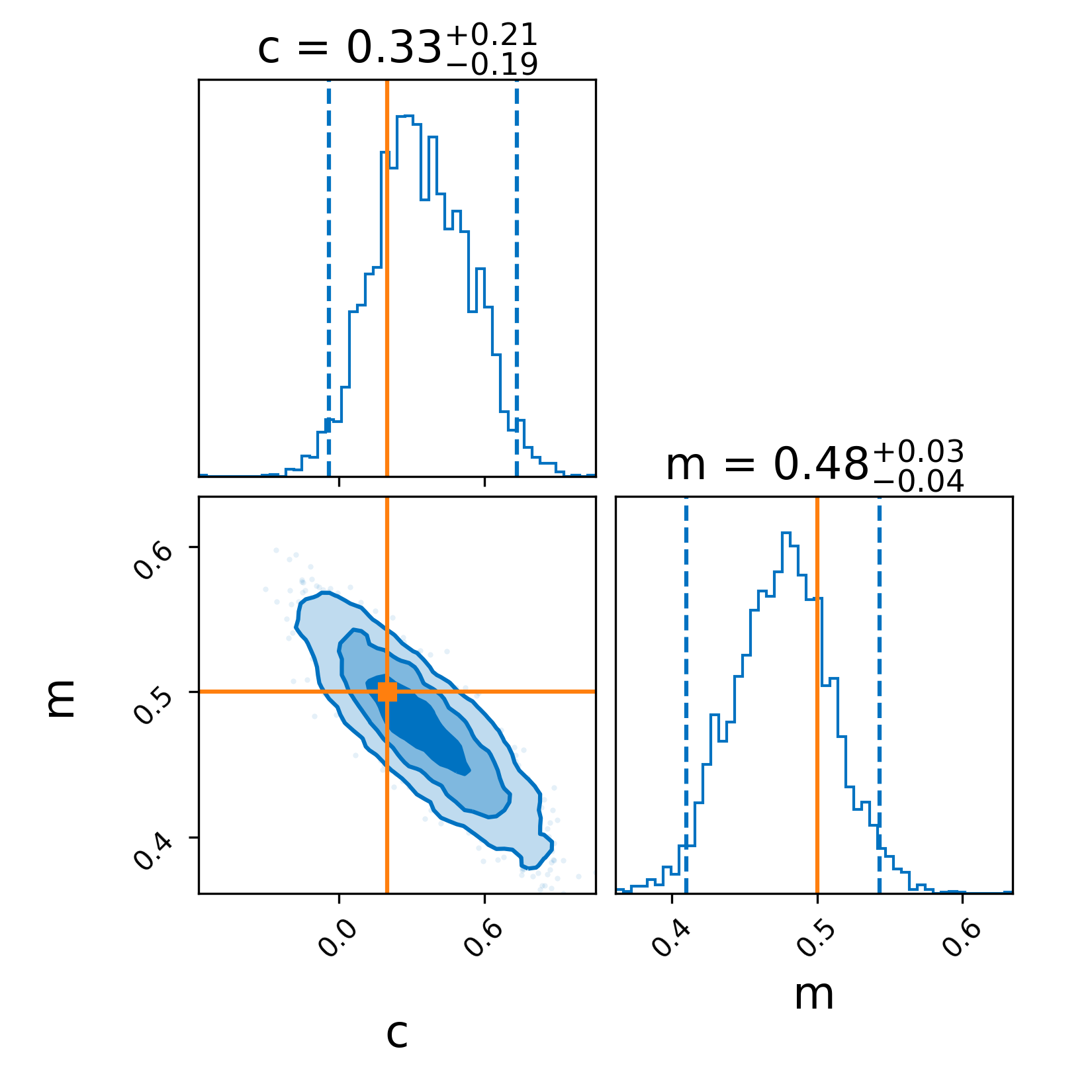

- docs/images/linear-regression_corner.png 0 additions, 0 deletionsdocs/images/linear-regression_corner.png

- docs/images/linear-regression_data.png 0 additions, 0 deletionsdocs/images/linear-regression_data.png

- docs/index.txt 1 addition, 0 deletionsdocs/index.txt

- examples/other_examples/linear_regression.py 1 addition, 1 deletionexamples/other_examples/linear_regression.py

docs/basics-of-parameter-estimation.txt

0 → 100644

docs/images/linear-regression_corner.png

0 → 100644

{kind=link}

110 KiB

docs/images/linear-regression_data.png

0 → 100644

{kind=link}

22.2 KiB